April 03, 2025

Market Update: The Trump Tariff Strategy

On Wednesday afternoon, President Trump unveiled his plan to impose baseline, and in some cases, reciprocal tariffs on all imported goods to the United States. The tariff rates were more aggressive than most investors expected, causing an abrupt response from the markets. Most risk assets—those that have a high potential for price volatility—sold off sharply on Thursday, with the S&P 500 down by 4.8%. The U.S. dollar dropped by more than 1.6%, supporting the translated returns from international holdings for domestic investors. Bonds showed their status as useful diversifiers, with the Bloomberg US Aggregate Bond Index up by 0.5%.

In our view, the dramatic increase in tariffs will slow growth and raise inflation over the short term, though we do not believe that is the administration’s end goal. Whether countries retaliate or negotiate will likely have the greatest influence on the long-term impact. We expect the news cycle to continue to be volatile over the coming weeks.

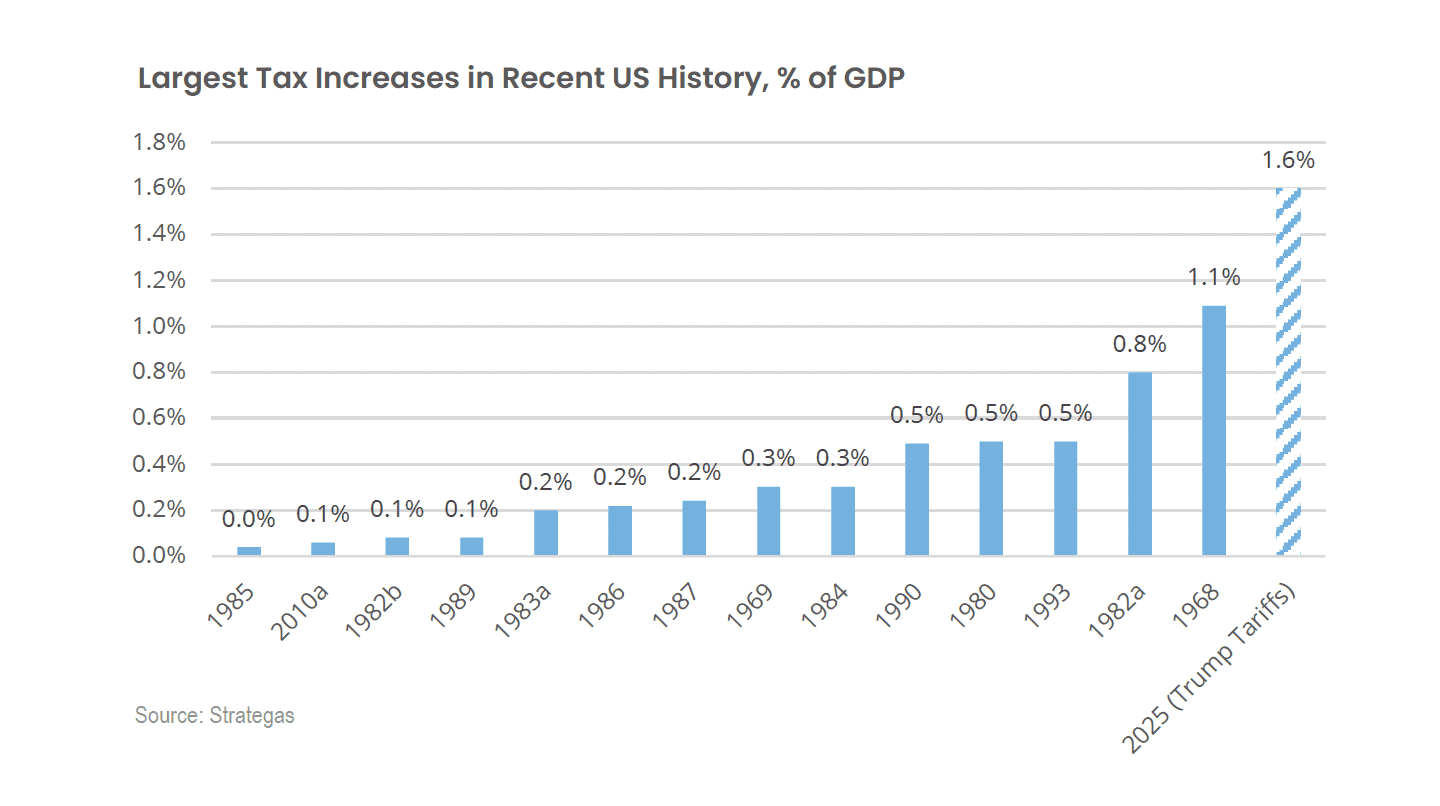

The Largest Tax Increase in U.S History

If fully enacted, the proposed tariffs would amount to the largest effective tax increase in modern U.S. history, equivalent to an estimated 1.6% of GDP. While we’ve argued that a onetime increase in prices isn’t inherently inflationary, it still erodes consumer purchasing power and is likely to dampen real economic growth. Although we have been skeptical of the Atlanta Fed’s GDPNow tracker, which suggests that the economy declined 2.8% in Q1, we believe that the tariffs alone could weigh heavily on growth through the remainder of the year.

Other Major Policies May Support Growth

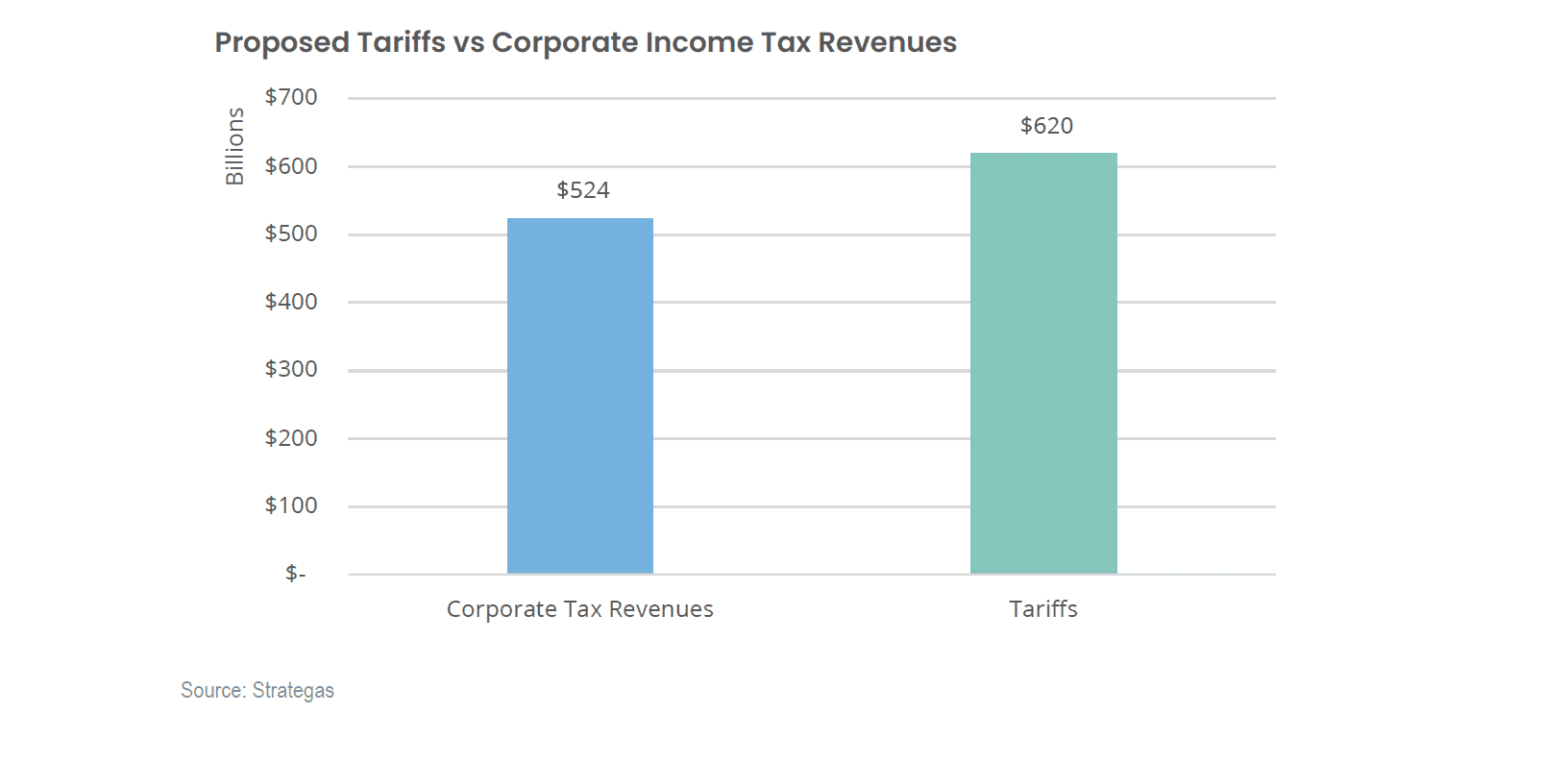

Importantly, the tariff plan is just one of the many policy initiatives promoted by President Trump. Including yesterday’s announcement, tariffs are anticipated to raise $600 billion in revenue this fiscal year, a figure that exceeds annual corporate tax receipts. It is likely that Congress adds elements to the budget resolution, in addition to the extension of the Tax Cuts and Jobs Act, that are stimulative. In addition, if the tariffs weaken demand significantly, the Fed may now be more likely to reduce interest rates. Several economists have increased their forecast for the number of rate cuts in 2025 as a result of the tariffs. All else being equal, lower rates should support equities.

What’s Next For Tariffs: Negotiations

We believe the administration took a harsher approach to tariffs so that they have the greatest leverage as they head into the negotiations phase with other countries. We’ve argued in the past that President Trump is more transactional than his predecessors. Although there is a risk that the opening offer is so aggressive that countries band together in blocks to counter the tariffs, they would also risk cutting off one of their most significant sources of income: the U.S. consumer. We believe it’s more likely to see them come to the table. Those negotiations are critical to understanding the administration’s long-term strategy. A series of deals that reduce tariffs from these proposed levels would be well received by the markets.

Diversifying Risk Exposures

We have long advocated for clients to hold portfolios that offer diversified sources of return. While the last few years have been dominated by the “fear of missing out” (FOMO) on the opportunity known as the Magnificent 7, the diversification strategy is paying off so far this year:

- International equities are holding strong, buoyed by both improving global growth and a weaker U.S. dollar.

- High-quality bonds are benefiting from attractive yields and a flight to safety.

- Alternative strategies are in many cases outperforming both equities and fixed income.

While Volatility is Uncomfortable, It Can Be Profitable

Market volatility can be unnerving in the moment, but corrections are a normal part of longterm investing. Historically, the S&P 500 has experienced 10% corrections in about 60% of calendar years and 15% corrections in roughly 40% of them. In the years that saw 10%–20% drawdowns, the average full-year return was still a solid 15%.

We do not believe volatility in markets is the same thing as risk. Instead, permanent loss of capital is what we strive to avoid, and fluctuating stock and bond prices often create opportunities.

Sentiment is particularly pessimistic right now, with fewer than 20% of individual investors expressing bullish views. As Warren Buffett famously reminds us: “Be fearful when others are greedy, and greedy when others are fearful.”

Parting Thoughts

In this environment, it’s worth remembering that the long-term return expectations embedded in financial plans are designed to include significant annual variations from both buoyant market periods (like 2023 and 2024) and challenging markets (like 2022) alike. We greatly appreciate your trust. If you have any questions or want to discuss anything in greater detail, please feel free to reach out.

The information provided is educational and general in nature and is not intended to be, nor should it be construed as, specific investment, tax, or legal advice. Individuals should seek advice from their wealth advisor or other advisors before undertaking actions in response to the matters discussed. No client or prospective should assume the above information serves as the receipt of, or substitute for, personalized individual advice.

This reflects the opinions of Focus Partners or its representatives, may contain forward-looking statements, and presents information that may change. Nothing contained in this communication may be relied upon as a guarantee, promise, assurance, or representation as to the future. Past performance does not guarantee future results. Market conditions can vary widely over time, and certain market and economic events having a positive impact on performance may not repeat themselves. The charts and accompanying analysis are provided for illustrative purposes only. Investing involves risk, including, but not limited to, loss of principal. Focus Partners' opinions may change over time due to market conditions and other factors. Numerous representatives of Focus Partners may provide investment philosophies, strategies, or market opinions that vary. The appropriateness of a particular investment or strategy will depend on an investor's individual circumstances and objectives.

Any index or benchmark discussed are for comparative purposes to establish current market conditions. Index returns are unmanaged and do not reflect the deduction of any fees or expenses and assumes the reinvestment of dividends and other income. You cannot invest directly in an index. This is prepared using third party sources considered to be reliable; however, accuracy or completeness cannot be guaranteed. The information provided will not be updated any time after the date of publication.

Services are offered through Focus Partners Wealth, LLC (“Focus Partners”), an SEC registered investment adviser with offices throughout the country. ©2025 Focus Partners Wealth, LLC. All rights reserved. RO-25-4378287